Is Sewer Line Repair Covered by Insurance? a 2026 Guide

You notice it in the middle of a normal day. The toilet starts gurgling after the shower drains. The kitchen sink empties slower than usual. Then you step outside and catch that unmistakable sewage smell near the yard.

At that point, most homeowners in Woodstock, Marietta, Roswell, or anywhere across North Metro Atlanta ask the same question. Is sewer line repair covered by insurance, or am I paying for this myself?

Here's the straight answer. Usually, no. Standard homeowners insurance often won't pay for the sewer pipe itself if the problem came from age, roots, corrosion, or a clog. That surprises a lot of people, and it creates a bad situation fast when you need sewer repair, sewer replacement, drain cleaning, or an emergency plumber near you.

What matters most is the cause of the damage, not just the fact that the sewer line failed. If you want a real shot at coverage, you need a clear diagnosis, fast documentation, and the right policy endorsements already in place.

The Unexpected Problem Beneath Your Yard

A sewer problem rarely starts with a dramatic collapse. Most of the time, it starts small and annoying.

Maybe your downstairs toilet in Acworth won't flush right. Maybe drains in your Canton home keep backing up after you've already tried plunging and store-bought drain cleaner. Maybe you see soggy ground in the yard, or you smell sewage near the cleanout line by the house. Those symptoms don't always mean a full sewer replacement is coming, but they do mean something is wrong below the surface.

The problem is that homeowners often treat the first warning signs like a routine clog. They search for "clogged toilet won't flush," "drain cleaning near me," or "emergency plumber Cumming," hoping it's a quick fix. Sometimes it is. Sometimes it isn't.

When the issue turns out to be the main sewer line, the stress changes immediately. Now you're not just dealing with a bad smell or slow drains. You're wondering whether the yard has to be dug up, whether the backup will get worse tonight, and whether your insurance company will cover any of it.

The first signs homeowners shouldn't ignore

These symptoms deserve quick attention:

- Repeated slow drains: More than one fixture draining slowly at the same time often points to a sewer line problem, not a single sink clog.

- Gurgling toilets: Air trapped in the system can signal blockage or damage in the main line.

- Sewage odor outside: A broken or leaking line can release odor into the yard.

- Wet spots in the lawn: If the ground stays soggy without rain, a sewer leak is on the list of possible causes.

- Backup at the lowest drain: When sewage shows up in a basement drain or lowest bathroom fixture, the main line needs to be checked.

If more than one drain acts up at once, stop thinking "simple clog" and start thinking "main line."

That shift matters. A sewer line problem is part plumbing emergency, part insurance issue. The plumber's diagnosis often decides whether you have a repair bill only, or a repair bill plus a possible claim.

Why Standard Homeowners Insurance Often Says No

A sewer line can be part of your home's plumbing and still fall outside standard coverage. That feels backward until you read how these policies are written.

Homeowners insurance usually pays for sudden, accidental damage tied to a covered peril. Sewer line claims often fail on that first test. If the carrier sees corrosion, age, root intrusion, buildup, or years of wear underground, it treats the problem as maintenance, not an insured loss. Bankrate explains that standard homeowners policies commonly exclude wear and tear, aging pipes, tree roots, and clogs, and it notes that coverage is more likely only when a separate covered peril caused the sewer damage in the first place, as outlined in its guide to whether homeowners insurance covers sewer line replacement.

What insurers are actually asking

The key question is simple. What caused the failure?

If a line collapses because old cast iron finally gave out, expect a denial. If roots entered through a weak joint over time, expect a denial. If the backup traces back to buildup that should have been cleared earlier, expect a denial. Homeowners in North Metro Atlanta run into this constantly, especially in older neighborhoods where aging materials and root-heavy lots are common.

That is why a real diagnosis matters more than a guess. A basic clog call and a proper sewer investigation are not the same thing. If the symptoms started with repeated backups or slow fixtures, get a plumber who can camera the line, identify the break, and document the location and cause. JMJ Plumbing handles that kind of professional drain cleaning and sewer clog diagnosis for North Metro Atlanta homeowners, and that documentation can make the difference between a supported claim and a fast denial.

The coverage gap homeowners miss

It's a common assumption that anything connected to the house is automatically covered by the main policy. It isn't.

Bankrate reports that a Nationwide survey found many homeowners wrongly believe service lines are covered under a standard policy. It also notes that even when a sewer-related loss qualifies under policy terms, the available limit may be capped under the policy structure rather than paid in full. In plain English, a qualifying event can still have a lower payout ceiling than you expect.

Practical rule: The insurer decides coverage based on cause first, then cost.

Do not hand the carrier a vague story like "the sewer line failed." Give them a timeline, the symptoms, camera findings, photos, and the plumber's written cause. Insurance companies look for prior issues, maintenance history, and anything that supports wear over sudden damage. The same pattern shows up in other claim disputes. Legal explainers on insurer investigations of disability claims are useful for that reason. They show how closely carriers examine history, records, and causation before they agree to pay.

Your Guide to Different Sewer Coverage Options

If you're trying to figure out whether sewer line repair is covered by insurance, stop thinking of it as one coverage question. It isn't. There are usually three separate buckets involved, and each one handles a different part of the mess.

One may help with a sudden covered loss. Another may help if sewage backs up into the house. A third may help with the underground line itself.

Comparing Sewer-Related Insurance Coverages

| Coverage Type | What It Typically Covers | What It Typically Excludes |

|---|---|---|

| Standard homeowners policy | Damage tied to a covered peril in limited situations | Gradual deterioration, aging, roots, corrosion, clogs, maintenance-related failure |

| Water backup endorsement | Sewage or drain backup damage inside the home, depending on policy wording | Repair of the broken exterior sewer line itself |

| Service line endorsement | Underground service line repair or replacement, depending on terms | Losses outside the endorsement terms, plus policy-specific exclusions and deductibles |

The biggest mistake I see homeowners make is assuming one add-on covers everything. It usually doesn't.

SelectQuote explains the key split clearly in its article on sewer line repair insurance and water backup coverage. Service line endorsements typically cover the underground pipe repair, while a separate water backup rider is needed for sewage overflow damage inside the home. Those riders often have separate limits and deductibles.

What each option means in real life

Let's make that practical.

If your sewer lateral cracks outside and causes recurring blockages, a service line endorsement is the coverage you hope you bought. If sewage backs up into your bathroom or finished basement, the interior cleanup may depend on a water backup rider. If a covered event damaged the line in a way your main homeowners policy recognizes, then the standard policy may come into play, but that situation is less common.

That means many homeowners need to review two separate add-ons:

- Service line coverage: For the buried pipe from the house toward the street.

- Water backup coverage: For the damage caused when sewage comes back into the home.

A lot of confusion around backup versus flood comes from sloppy use of the word "water." Insurance agencies in other regions explain this distinction well. This breakdown of water damage explanations for Alabamians is useful because the principle is the same anywhere. Sewer backup, plumbing overflow, and flood are not the same claim category.

What to look for in your policy today

Pull your policy and check the declarations page. Don't skim it. Look for the actual endorsements listed.

Focus on these questions:

- Is service line coverage listed by name? If not, don't assume it's there.

- Is water backup coverage separate? It often is.

- What deductible applies? It may differ from your main homeowners deductible.

- What restoration is included? Pipe repair, excavation, and surface restoration may not all be treated the same.

- Are there cause-based exclusions? Read the wording on wear, roots, corrosion, and maintenance.

If you're dealing with recurring clogs and need to rule out a simple blockage before you panic about replacement, start with a proper drain cleaning and toilet clog service. Sometimes the issue is in the drain system. Sometimes that service is what confirms the problem is farther out in the main sewer line.

How to Document Damage and File Your Claim

When sewage is backing up or the yard smells like a septic trench, the immediate impulse is to jump straight to repair. That's understandable. But if you want any chance of insurance help, slow down just enough to document the problem correctly.

The claim lives or dies on evidence. Not guesses. Not a phone call saying "something's wrong underground."

Start with damage control

Your first job is to prevent things from getting worse.

If sewage is entering the home, stop using water fixtures that drain into that line. That means toilets, showers, washing machines, and sinks tied to the affected branch or main line. Then call a licensed plumber who handles sewer backup and emergency plumbing.

This is where fast diagnostics matter. A camera inspection can identify whether the problem is roots, a belly in the line, scale buildup, separation, collapse, or a clog. If you need that kind of proof, a sewer camera inspection gives the homeowner and the insurer a much clearer picture of the line condition.

Document before major work begins

Take photos and video before excavation or heavy cleanup changes the scene.

Capture:

- Interior backup evidence: Toilets, tubs, showers, floor drains, and affected flooring.

- Exterior signs: Wet ground, sink areas, exposed cleanouts, or sewage odor zones if visible conditions support that.

- Fixture behavior: Short videos of bubbling toilets or slow drainage can help show system-wide symptoms.

- Anything removed from the line: Roots, debris, broken pipe segments, or displaced material if the plumber retrieves them.

Don't rely on memory. Photograph the problem before anyone starts digging or hauling debris away.

Get a written diagnosis that names the cause

This is the step many online guides miss. The plumber's report is not just for the repair file. It's often the backbone of the insurance conversation.

Ask for documentation that identifies:

- Where the failure is located

- What caused it

- Whether the condition appears sudden or long-developing

- Whether backup damage occurred inside the home

- What immediate repair or replacement is necessary

A vague invoice that says "cleared line" won't do much for a claim. A detailed report with camera findings, photos, and cause assessment is far more useful.

Call your insurer with facts, not assumptions

Once you have documentation, contact your agent or claims department. Tell them what happened, where it happened, and what the plumber found. Ask specifically whether the policy includes service line coverage, water backup coverage, or both.

If the representative speaks in generalities, push for specifics. You need to know which part of the loss you're discussing:

- pipe repair,

- excavation access,

- landscaping restoration,

- interior water damage,

- cleanup and sanitation.

If the answer is no, ask them to point to the policy language. If the answer is maybe, keep every record.

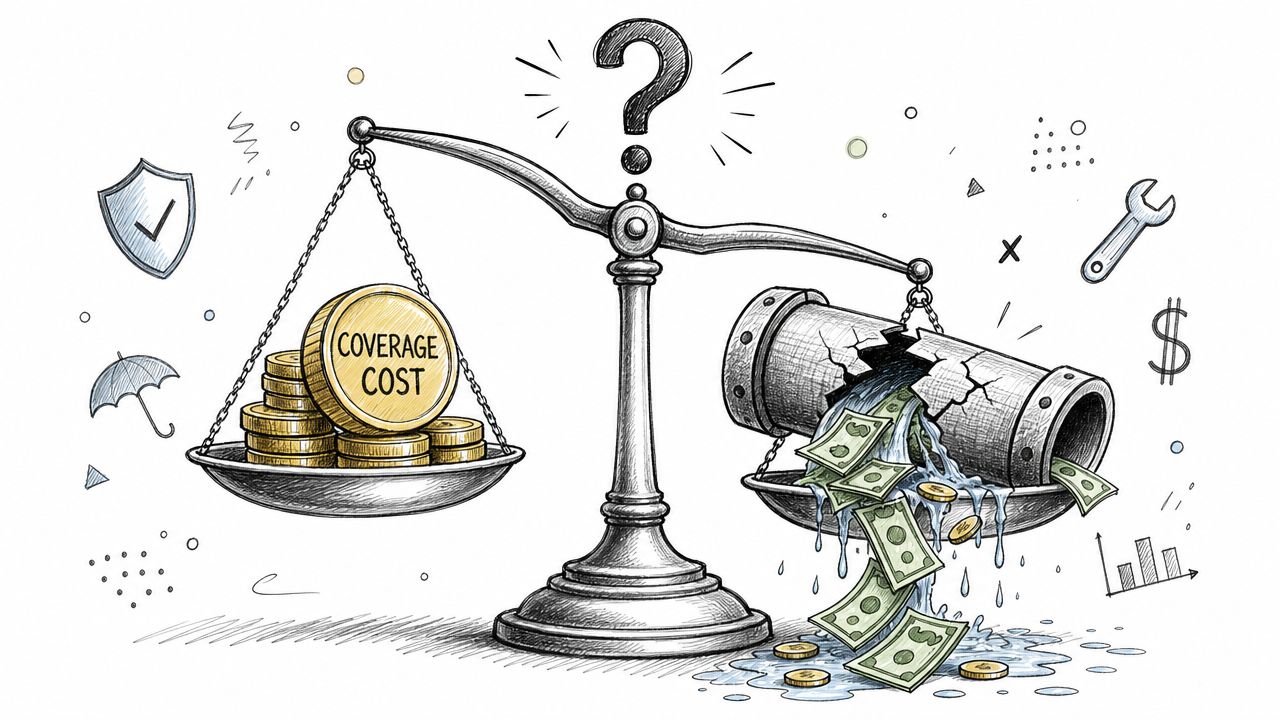

Is Extra Sewer Line Coverage Worth the Cost

A sewer line can look fine for years, then fail on a weekend after heavy use, and suddenly you are choosing between a five-figure repair and a hard conversation with your insurer. That is the real question here. Can you afford a bad sewer line problem out of pocket?

What the available data actually says

Consumers' Checkbook reported that one insurer filing with the California Department of Insurance showed an average sewer-line-coverage claim of $430 in 2015, according to Checkbook's review of water and sewer line warranties and claim frequency.

The same Checkbook review said another utility partnership reported claims averaging about $580, and only 0.7% of customers per year filed sewer-line claims.

Those numbers matter, but they do not settle the decision by themselves. Low claim frequency does not help much if your line collapses and you are the one writing the check.

Checkbook also found warranty plans often cost $4 to $13 per month. In many cases, service line endorsements through homeowners insurance run roughly $30 to $160 per year, often with a $500 deductible. Major excavation and replacement jobs can exceed $10,000 to $20,000. That gap between annual premium and worst-case repair cost is the only reason this coverage deserves a serious look.

Who should seriously consider it

I recommend extra sewer line coverage for homeowners who have a real chance of facing a costly failure, not for people buying every add-on out of fear.

It makes sense if any of these fit your house:

- Your home is older. Older sewer materials fail more often from corrosion, shifting, and joint separation.

- You have large trees between the house and the street. Roots keep finding weak spots.

- Your sewer lateral is long. More buried pipe means more places for trouble to start.

- A backup would damage a finished basement or lower level. The repair bill is only part of the loss.

- You do not want to self-insure a sudden underground repair. That is a valid reason to buy the endorsement.

For many North Metro Atlanta homeowners, this is not theoretical. Older neighborhoods in Marietta, Roswell, and parts of Canton can have aging lines. Homes in Alpharetta, Johns Creek, and Woodstock often have mature landscaping that puts pressure on buried piping. Local conditions change the math.

When the coverage is a bad buy

Skip it if the endorsement is narrow, the deductible wipes out the likely benefit, or the exclusions are broad enough to block the failures your property is most likely to have.

Read the fine print with a hard eye. Does it cover the pipe itself, excavation, access, and restoration, or just one piece of the job? Does it exclude wear, roots, ground movement, or pre-existing damage? Those exclusions decide whether the policy helps when you need it.

My advice is simple. Buy coverage for rare, expensive sewer failures. Do not buy it expecting routine drain service or every underground problem to be paid.

If you are in North Metro Atlanta and you are unsure whether your risk is high or low, get a diagnosis before you guess. A camera inspection and written cause report from a local plumber often tells you more than the sales page for the endorsement. If the line is already acting up, start with emergency sewer and plumbing help in North Metro Atlanta and get the facts before you decide whether extra coverage belongs in your budget.

Your Local Sewer Repair Partner in North Metro Atlanta

North Metro Atlanta homes don't all fail the same way. An older property in Marietta may have aging underground piping. A yard in Alpharetta or Johns Creek may have mature roots pushing toward line joints. A home in Woodstock or Acworth may start with what looks like a simple drain issue, then turn into a full main line diagnosis.

That's why local context matters. Soil conditions, tree cover, home age, and line length all affect how sewer problems show up and how quickly they become emergencies.

What homeowners need when the line fails

In a sewer emergency, you need more than someone to snake a drain and leave.

You need a plumber who can determine whether the problem is a stoppage, a break, root intrusion, corrosion, separation, or collapse. You also need documentation that supports the next step, especially if you're trying to deal with an insurance carrier.

For North Metro Atlanta homeowners searching for an emergency plumber in Cumming, a 24 hour plumber in Acworth, sewer repair in Woodstock, or sewer replacement near Marietta, the first move should be a fast diagnosis. That tells you whether you're dealing with a temporary clog, a repairable section, or a replacement decision.

Why the first call matters

A rushed first visit can create confusion later. If nobody documents the cause, the timeline, and the visible damage, your insurance conversation gets weaker. If the wrong repair gets done first, you may spend money without solving the actual problem.

One practical option for homeowners in this area is JMJ Plumbing's emergency plumbing service, which handles sewer backups, leak emergencies, and urgent diagnostic work in North Metro Atlanta. The important part isn't the brand name. It's the sequence. Get the line assessed quickly, get the cause documented, and then decide whether you're filing a claim, approving repair, or both.

If you smell sewage in the yard, have multiple slow drains, or need a sewer repair near you tonight, don't wait for the problem to "settle down." Sewer issues usually move in the opposite direction.

Frequently Asked Questions About Sewer Insurance

Does insurance cover tree root damage in a sewer line

Usually not under a standard homeowners policy. Root intrusion is commonly treated like maintenance, wear, or gradual damage. If you bought service line coverage, review that endorsement carefully to see whether root-related damage is included or limited.

Is a sewer backup the same as flood damage

No. These are usually separate insurance issues. Sewer or drain backup may fall under a water backup rider. Flooding from rising external water usually requires flood insurance, not a standard homeowners policy.

What should I do if my sewer claim is denied

Ask for the denial in writing and request the policy language the carrier relied on. Then review your plumber's diagnosis, camera findings, photos, and endorsements. If the denial seems to ignore the actual cause of loss or the endorsements you bought, escalate with your insurer and consider professional advice.

If you're dealing with slow drains, sewage smell, yard saturation, a sewer backup, or you're trying to figure out whether your sewer line repair is covered by insurance, contact JMJ Plumbing. They serve North Metro Atlanta with 24/7 plumbing response, sewer diagnostics, repair and replacement, and the documentation homeowners often need before they can make a solid insurance claim.